Latest News

Blog

Portfolio Perspectives: Tech Stocks, IPOs, and Higher Interest Rates

May 26, 2026

The S&P 500 recently surpassed 7,500 for the first time, marking another milestone in a year that has seen many new all-time highs. This is positive for clients, especially because several sectors have contributed to this rally. These trends have also fueled enthusiasm for IPOs, particularly ones related to artificial intelligence, after years of relatively few companies going public.

This is occurring despite ongoing concerns over inflation, high oil prices, and hopes for a peace deal in Iran that has not yet materialized. In contrast to the stock market, these challenges have weighed on the bond market, pushing long-term interest rates higher. The 30-year U.S. Treasury yield, for instance, briefly reached a nearly 20-year high before settling back toward 5%. Since headlines like these can create uncertainty for markets, maintaining perspective and balance are more important than ever.

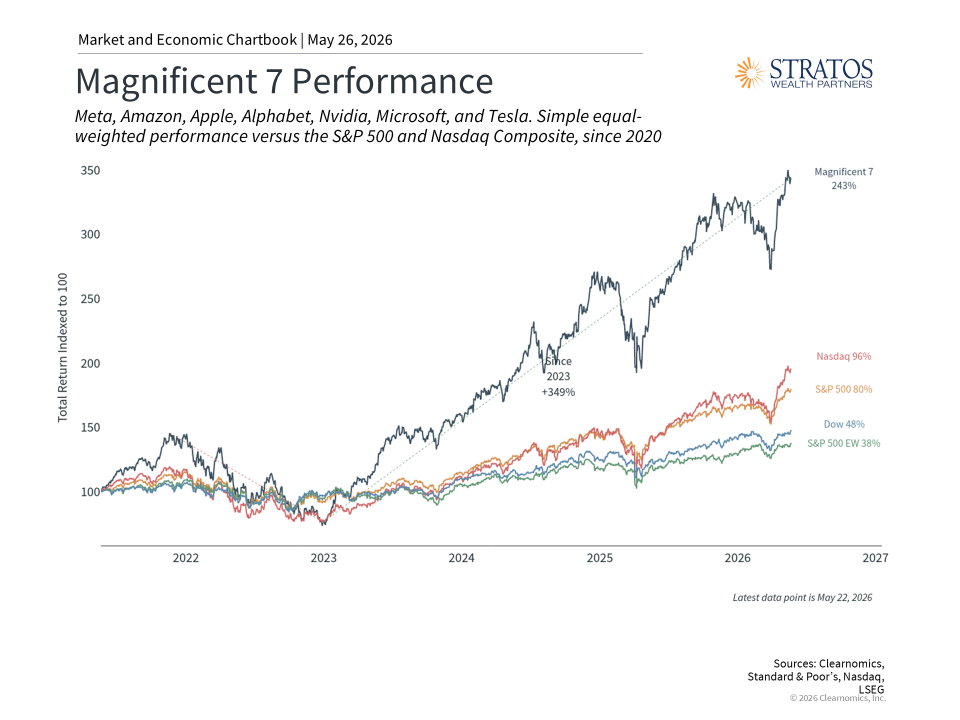

Technology stocks continue to support market performance

While the energy sector continues to lead the market, technology-related stocks have also contributed to portfolio returns this year. The Magnificent 7, which includes Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, and Tesla, now represents about 35% of the S&P 500. This emphasizes the importance of portfolio construction, since some investors may not realize how much exposure they may have to these individual companies today.

What has supported the market rally is not just positive sentiment, but also strong fundamentals. S&P 500 earnings growth has been running well above its historical average, and many of these large companies have continued to deliver positive earnings surprises. Current consensus earnings estimates suggest that the Information Technology and Communication Services sectors could grow earnings by 35.8% and 17.3%, respectively, over the next year.1 Other sectors, including Materials and Energy, are expected to experience above-average growth as well.

That said, valuations have also climbed alongside prices. The S&P 500 forward price-to-earnings ratio currently sits near 21x, above the historical average of 16x. Technology stocks specifically trade at a forward P/E around 24x.2 While elevated valuations do not predict short-term market moves, they are an important consideration for clients thinking about asset allocation. Maintaining balance across sectors, sizes, and styles can help manage risk while also benefiting from market trends.

IPO activity is returning to public markets

The stock market is constantly evolving, since existing companies can be acquired, merged with others, or in some cases fail. At the same time, new companies can join major exchanges through a process known as an initial public offering, or IPO.

This is one reason why the opportunity set available to investors today looks different than it did even a decade ago. For example, while the FT Wilshire 5000 was originally designed to include roughly 5,000 publicly traded U.S. companies, today it contains only about 3,400 components.3 This reflects a long-term trend of companies staying private for longer.

Recently, headlines have focused on a number of high-profile companies that are reportedly considering public offerings, including SpaceX, Anthropic, OpenAI, and others.4 Many of these are large businesses that have grown primarily through venture capital and private investment rather than public markets. From that perspective, these potential IPOs are positive because they make shares of these companies available to a broader set of investors. Stock market indices automatically incorporate new public companies as they grow, meaning that long-term investors gain exposure to successful IPOs over time without needing to invest in them directly at the time of offering.

Of course, what captures the attention of many clients are the headlines and excitement surrounding IPOs. For some, it is natural to wonder whether participating in an IPO is an opportunity for early gains. However, this is not always the case. For instance, it’s often the institutional investors and company insiders that truly participate in the IPO itself, and many have often been invested for years before the public offering. Additionally, these company insiders are often subject to lock-up periods, commonly 180 days, during which they cannot sell their shares. When these periods expire, additional selling pressure can weigh on the stock price, sometimes catching clients by surprise.

IPO activity tends to come in waves, often occurring during strong economic periods when investment capital is plentiful and market enthusiasm is high. The dot-com boom of the late 1990s is perhaps the most famous example, but there are many other periods as well. For example, the post-pandemic market recovery experienced a jump in Special Purpose Acquisition Company (SPAC) activity, which is one way some companies can go public. This wave was relatively short-lived, demonstrating the importance of maintaining a longer-term perspective.

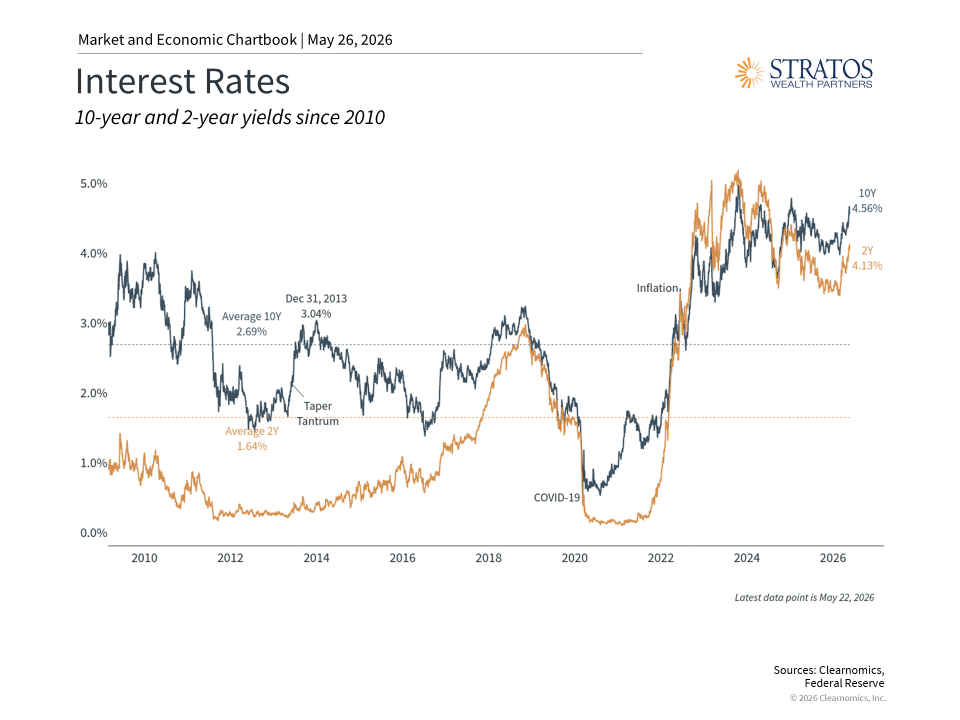

Long-term interest rates have remained elevated

While the stock market has been climbing to new highs, long-term interest rates have also been rising. This is primarily due to inflation concerns, complicating the path of Fed policy over the next year. Technology stocks are typically sensitive to interest rates and inflation since they affect the value of their future cash flows. This is one reason these stocks struggled in 2022 as interest rates spiked, and then performed well as inflation moderated in the years since.

Beyond the technology sector, higher interest rates have implications across the economy and markets. Mortgage rates have moved up, with the 30-year fixed rate now around 6.5%, above the long-term average of 6.02% since 1990. This affects housing affordability and broader real estate activity. Higher rates also influence the cost of capital for businesses and the discount rate applied to future earnings, which can affect stock valuations, particularly for growth-oriented companies whose value depends heavily on future cash flows.

At the same time, higher interest rates mean that bonds are now offering more meaningful income than they have in many years. Investment grade corporate bonds yield 5.3%, compared to a long-term average of 3.8%. Treasurys yield 4.4%, well above their historical average of 2.2%.5 For investors, this creates more attractive opportunities in fixed income, which can play a more meaningful role in diversified portfolios going forward.

The bottom line? While the stock market has reached new milestones this year, rising interest rates serve as a reminder that the broader economic environment may present future challenges. For long-term investors, the best approach is to maintain a balanced portfolio that can benefit from market growth as well as higher interest rates.

References

- Clearnomics research and LSEG data as of May 20, 2026

- Ibid.

- https://cdn.prod.website-files.com/63e3e50fdce0bcaff7861530/6965694be133b820fb1f390d_FT%20Wilshire%205000%20Index%20Series%20Factsheet%20v2%20-%20Dec%202025.pdf

- https://www.wsj.com/topics/subject/initial-public-offerings-ipos

- Bloomberg U.S. Corporate Investment Grade and Bloomberg U.S. Treasury Index yields, as of May 22, 2026

Index Descriptions

S&P 500

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The modern design of the S&P 500 stock index was first launched in 1957. Performance prior to 1957 incorporates the performance of the predecessor index, the S&P 90.

NASDAQ

The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index.

Taylor Salisbury is a registered representative with, and securities offered through LPL Financial, member FINRA/SIPC. Investment advice offered through Stratos Wealth Partners, Ltd., a registered investment advisor. Stratos Wealth Partners, Ltd. is a separate entity from LPL Financial.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal professional.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.

This material was prepared by Clearnomics, Inc., who is not affiliated with the named financial professional, firm or broker/dealer.

Tracking ID: #1114749

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.