Latest News

Blog

Advanced Estate Planning to Optimize the Transfer of Family Wealth

May 29, 2026

For many people, the wealth they have accumulated over a lifetime is more than just about money. It represents years of hard work, discipline, and sacrifice to ensure they can have a comfortable retirement, take care of their families, and more. Yet, one of the most important and often overlooked questions in financial planning is not how to grow wealth, or even how to spend it, but how to pass it on efficiently and intentionally. This requires thoughtful estate planning that covers a breadth of financial planning topics including taxes, goals, and the concept of legacy.

Despite its importance, a 2025 survey found that fewer than one in three Americans report having a will, and more than half say they have no estate plan at all.1 This gap between intention and action is significant. Without a thoughtful structure in place, wealth that took decades to build can be eroded by taxes, legal complications, and unintended distributions. Advanced estate planning addresses this challenge by creating a coordinated approach designed to maximize the efficient transfer of assets to the people and causes that matter most.

At its core, estate planning serves two broad purposes. First, it supports non-financial goals, such as meeting the needs of dependents, protecting assets from creditors, and ensuring that assets pass to the right people in the right way. Second, it optimizes financial goals such as managing tax obligations, maintaining liquidity, and preserving the value of business interests. The most effective plans integrate both types of goals and treat wealth transfer as a long-term and continuous process.

Establishing the right framework for wealth transfers

Before exploring specific strategies, it is worth understanding the foundational decisions that shape every estate plan. These begin with three simple but important questions: what assets are being transferred, to whom are they being transferred, and when will this transfer occur?

The type of assets being transferred matters because it influences which transfer strategies are most appropriate. Assets such as cash and publicly traded securities, including typical stocks and bonds, are the most straightforward to transfer because they are liquid. Real estate, closely held business interests, and alternative investments introduce complexity because they are harder to value and may be difficult to divide among multiple beneficiaries.

Every estate plan begins with creating a picture of who will benefit from the assets being transferred. Beneficiaries can include a spouse, children, grandchildren, other relatives, close friends, or charitable organizations. Each beneficiary type may call for different planning strategies, particularly when balancing the needs of a surviving spouse against the long-term interests of children or future generations. Identifying beneficiaries early in the planning process helps ensure that the right assets reach the right people in the most effective way.

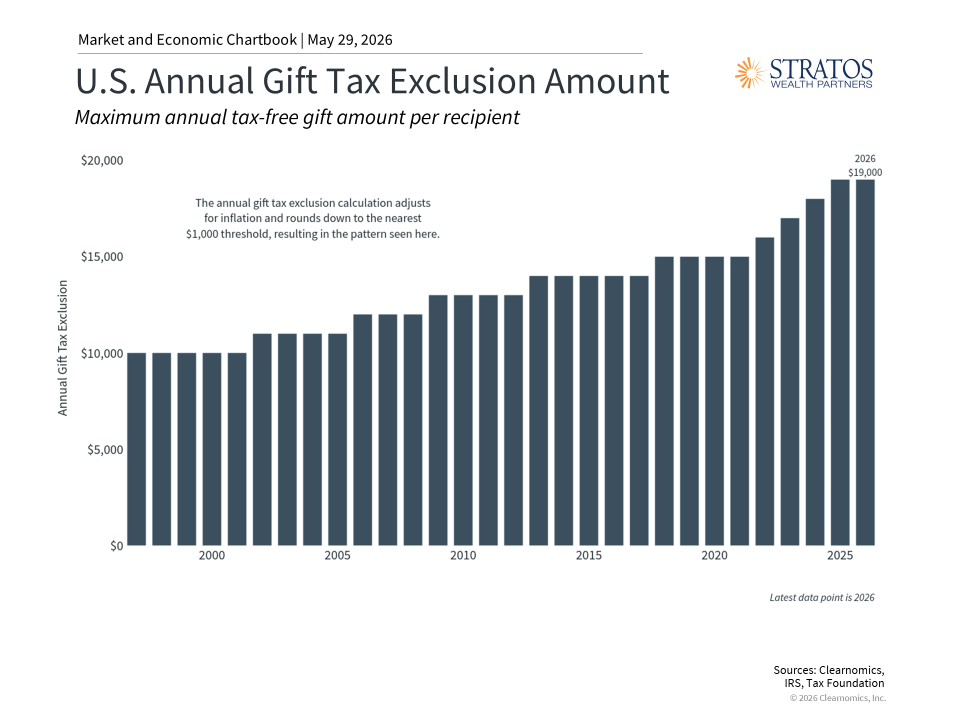

The timing of asset transfers is another key consideration. Some assets pass directly to beneficiaries upon death, while others may be strategically distributed over time. For example, by making “completed gifts” over one’s lifetime, a donor can take advantage of annual gift exclusions to increase the amount of tax-free transfers.

In 2026, the annual gift exclusion is $19,000 per recipient, meaning a donor can transfer property up to that amount to any one individual or $38,000 if splitting the gift with their spouse without paying taxes.2 Executed over time, this approach can remove a significant portion of taxable estate value and allows for greater intention over how and when beneficiaries receive their inheritance.

Transfer strategies for different goals

With an understanding of these foundational elements, the next step is identifying the goals that can be achieved through estate planning and mapping them to the options available. Here are some examples:

Reducing the taxable value of the gross estate

- For individuals seeking to minimize estate taxes due while transferring future appreciation to the next generation, they can reduce the value of their gross estate and ensure their beneficiaries receive distributions through irrevocable trusts.

- A common example is a Grantor-Retained Annuity Trust, or GRAT, where the grantor transfers assets into the trust and receives annuity payments over a set term.

- If the grantor survives the trust term, the remaining assets pass to beneficiaries outside of the taxable estate, though care needs to be taken as gift taxation can apply.

Achieving philanthropic goals

- For families with philanthropic goals, another option for reducing estate value is a Charitable Remainder Trust, or CRT.

- This option allows the grantor to designate beneficiaries to receive the income interest for a set term and have the remainder go to a designated charity. In addition to removing assets from the gross estate, this method provides a gift tax and income tax deduction for the charitable remainder interest.

- CRTs work well with highly appreciated assets that may generate capital gains tax, such as real estate or concentrated stock. Within the trust, the proceeds are reinvested in a diversified portfolio, and the beneficiary receives an income stream for life or a specified term. This approach converts a low-yield, high-gain asset into a tax-advantaged income stream while achieving philanthropic aims.

Managing business interests

- For families with business interests or other illiquid assets, additional planning around liquidity, governance, and continuity is essential.

- Buy-sell agreements specify how ownership transfers if an owner passes away or becomes incapacitated, preventing disputes and ensuring that the business can continue operating.

- Key-person life insurance can provide liquidity to cover ongoing business operations or fund a buyout without requiring a forced sale of the business.

- Family Limited Partnerships, or FLPs, allow senior family members to create different classes of ownership and transfer ownership interests to the next generation while retaining control as the general partner. Because limited partnership interests lack control and marketability, they may be eligible for valuation discounts allowing families to transfer more value within the gift and estate tax exemption limits. Asset protection is an additional benefit, shielding family members from the claims of outside creditors. This structure is especially valuable in the context of a family business, where continuity of management is as important as tax efficiency.

Planning for Wealth Transfers is a Continuous Process

Like all financial planning activities, estate planning is a lifelong process that requires monitoring and adjustments as personal circumstances and fiscal policies change.

A common example of changing personal circumstances is the growth of families. An estate plan that is optimized for a young family will naturally need to be revisited as that family ages and grows. When multiple future generations are involved, the complexity of wealth transfers to those beneficiaries also increases.

The Generation-Skipping Transfer Tax (GSTT) is relevant in these situations since it was implemented to ensure that transfers are taxed at each generation, and thus applies to transfers to recipients that are two or more generations younger than the donor. With careful planning, a donor can reduce or avoid this additional transfer tax through various transfer techniques.

Finally, policy changes can reshape outcomes over time. Federal estate and gift tax exemptions have shifted significantly across administrations, from as low as $675,000 in 2001 to a high of $15 million per individual today.3This was put in place by the 2017 Tax Cuts and Jobs Act when it doubled the exemption, and the One Big Beautiful Bill made these higher thresholds permanent.

State-level rules add another layer of complexity, since some states impose their own estate or inheritance taxes with different exemption thresholds than the federal level. Residency and domicile decisions can therefore have meaningful financial consequences for some families. It is important to stay current on any policy changes that ultimately affect the estate tax calculation.

All of these strategies work best when they are integrated with one another and with broader lifetime gifting and philanthropic goals. And, as with all areas of financial planning, the key to success is to start as early as possible, and to continuously refine your plan so it aligns with your goals.

The bottom line? Estate planning requires a coordinated approach designed to preserve wealth, reduce taxes, and ensure that assets reach the right people, in the right way, at the right time.

References

- https://www.caring.com/resources/wills-survey

- https://www.irs.gov/businesses/small-businesses-self-employed/whats-new-estate-and-gift-tax

- https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill

Taylor Salisbury is a registered representative with, and securities offered through LPL Financial, member FINRA/SIPC. Investment advice offered through Stratos Wealth Partners, Ltd., a registered investment advisor. Stratos Wealth Partners, Ltd. is a separate entity from LPL Financial.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal professional.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.

This material was prepared by Clearnomics, Inc., who is not affiliated with the named financial professional, firm or broker/dealer.

Tracking ID: 1117049

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.