Latest News

Blog

Reasons to Be Thankful This Holiday Season

November 17, 2025

Taylor Salisbury, CFP® | Partner & Private Wealth Manager

With the holiday season upon us, now is an excellent opportunity to reflect on and value what we possess, in both our personal circumstances and financial portfolios. This reflection is especially valuable given investors’ natural tendency to concentrate on potential risks rather than celebrating achievements. Currently, as markets show positive performance, taking time to review the past year offers valuable perspective while new challenges and opportunities continue to develop.

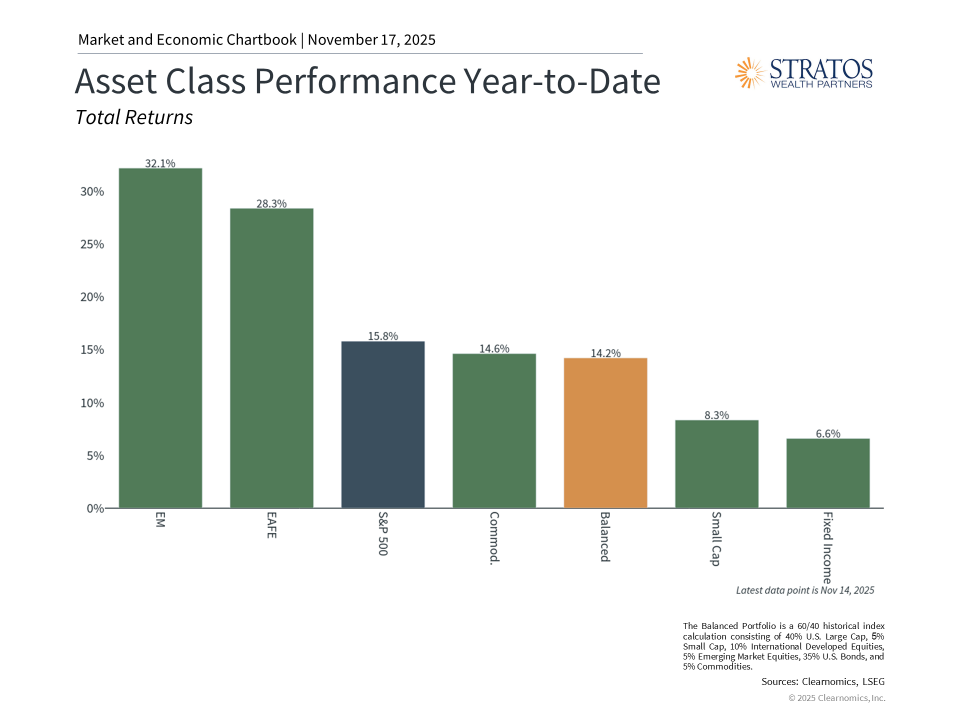

Throughout history, financial markets have provided robust returns, and the current year has followed this pattern. Year-to-date, the S&P 500 has risen more than 15% including dividends, while the Bloomberg U.S. Aggregate Bond Index shows bonds have delivered roughly 7% returns. For the first time in several years, international equities have surpassed U.S. stock performance. Numerous diversified portfolios have gained from this widespread positive performance spanning multiple asset classes. What considerations should investors bear in mind while preparing for the upcoming year?

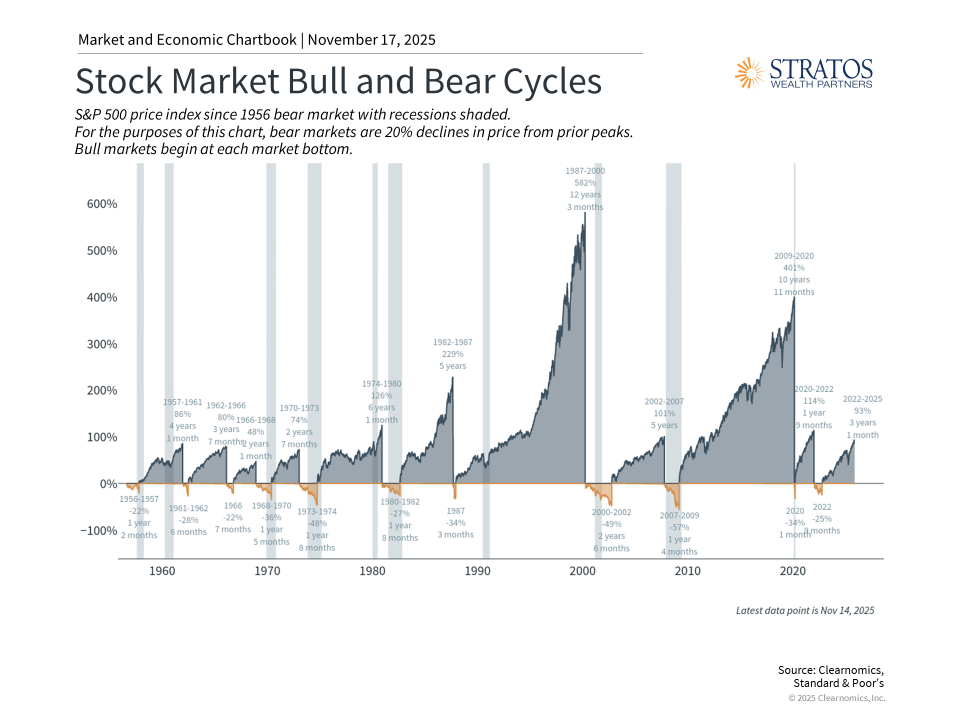

The bull market has reached its fourth year

To begin with, clients have reason for gratitude that financial markets have shown solid performance throughout this year despite periods of volatility. The current bull market cycle, which commenced following the market trough in October 2022, has now progressed into its fourth year.

Although historical performance doesn’t guarantee future outcomes, the record indicates that bull markets typically extend considerably longer than bear markets, frequently continuing for five to ten years or beyond. Historical bull markets have generated cumulative returns that substantially exceed what this cycle has produced thus far, even when investors encountered numerous obstacles during those periods. While legitimate concerns exist regarding valuations and market concentration, long-term investing necessitates successfully navigating various market conditions.

The bond market’s favorable returns deserve recognition following the difficult interest rate and inflation climate of recent years. With rates achieving stability and the Federal Reserve resuming monetary policy easing, bond valuations have improved. This illustrates why maintaining positions in both stocks and bonds continues to be essential for portfolios regarding both equilibrium and income production.

This strength reinforces a crucial principle: attempting to time markets based on near-term events proves not only challenging but potentially harmful when not evaluated within your comprehensive financial plan. This held true even during April when markets declined nearly to bear market territory following new tariff announcements. Markets rebounded swiftly and subsequently reached fresh all-time peaks. Investors maintaining discipline received rewards, whereas those responding to news coverage potentially missed opportunities and, in certain instances, might remain uninvested.

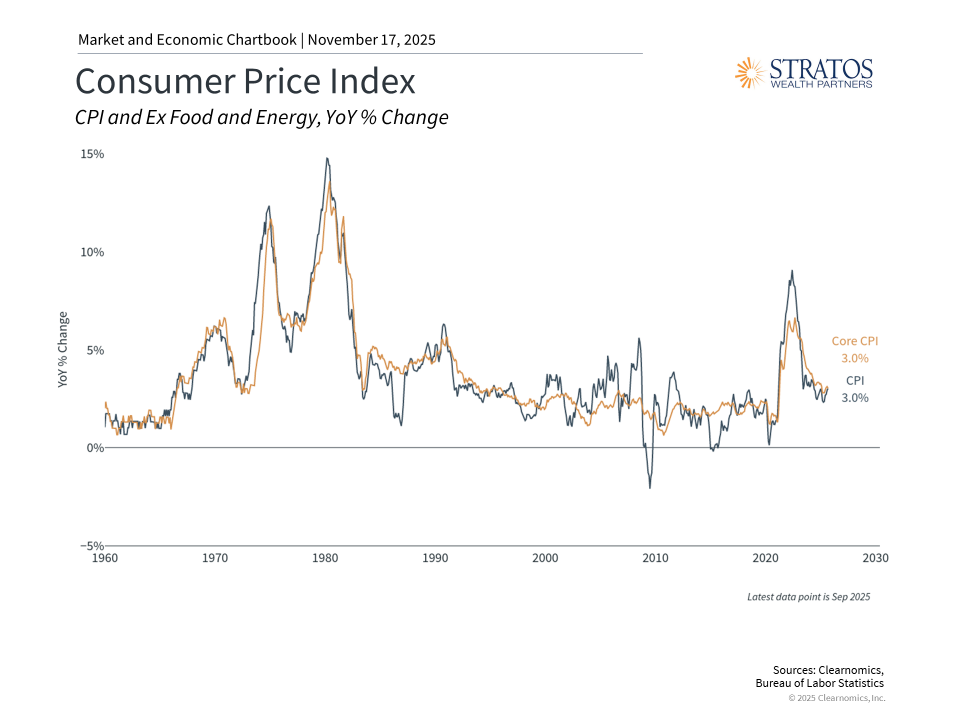

Inflation has moderated and the Federal Reserve is reducing rates

Additionally, clients can express appreciation that inflation has moderated, despite progress occurring more gradually than many anticipated. Over the past year, prices have increased approximately 3%, which continues presenting difficulties for households and policymakers. From an investment perspective, however, inflation has demonstrated considerably more stability, with diminished concerns about accelerating inflation relative to previous years.

This situation has enabled the Fed to initiate interest rate reductions following an extended period of maintaining restrictive levels throughout most of the year. Rate cuts also aim to bolster the employment market, which has shown weakness since summer. Historical patterns indicate that declining rates benefit stocks and bonds alike through reduced borrowing expenses for businesses and consumers while enhancing the value of existing bonds carrying higher interest rates. Therefore, while inflation and interest rates will continue as significant market factors, concerns about perpetually rising inflation and interest rates seem to be in the past.

Asset allocation facilitates risk management while seizing opportunities

Lastly, clients should recognize the significance of continuous risk management and appropriate asset allocation. The coming year will probably introduce fresh sources of uncertainty, as every year typically does. When uncertainty arises, concerns about recessions, bear markets, and potential cycle endings naturally emerge. Instead of responding to each market development, long-term investors can maintain suitable portfolios capable of navigating various phases of market and economic cycles.

We can also express gratitude for having diverse assets available that help balance risk and potential returns. Risk management remains critical throughout an investor’s journey, particularly following a three-year market rally. The S&P 500 price-to-earnings ratio of 22.6x exceeds historical averages and gradually approaches its peak dot-com era levels.

While valuations don’t forecast near-term market direction, meaning markets can potentially continue performing well, they do indicate that future returns might prove more moderate, especially relative to more attractively valued asset classes and sectors. Consequently, maintaining realistic expectations and holding various market segments with more favorable valuations becomes important.

Questions surrounding artificial intelligence will continue. Given the transformative nature of this technology, difficulty in predicting its impact on stock valuations is understandable. This parallels the challenges of forecasting how the internet revolution would develop starting in the mid-1990s. Political volatility will probably persist with continuing tariff modifications, geopolitical concerns, the expanding national debt, and additional factors. Recent experience confirms that overreacting to these developments proves not only counterproductive but capable of disrupting financial plans.

The bottom line? The holiday season provides an opportune moment to contemplate numerous reasons for gratitude and examine your portfolio composition. A well-constructed portfolio balances the advantages of various asset classes while directing them toward financial objectives. This approach remains essential for successfully navigating both challenges and opportunities in the coming year.

Taylor Salisbury is a registered representative with, and securities offered through LPL Financial, member FINRA/SIPC. Investment advice offered through Stratos Wealth Partners, Ltd., a registered investment advisor. Stratos Wealth Partners, Ltd. is a separate entity from LPL Financial. Trading instructions sent via email, fax, or voicemail will not be honored. There is no assurance that these messages can be retrieved on a timely basis, nor is there any sure method of confirming the customer identity. The information contained in this message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying of this message is strictly prohibited. If you have received this message in error, please immediately delete.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

Tracking ID: 826892